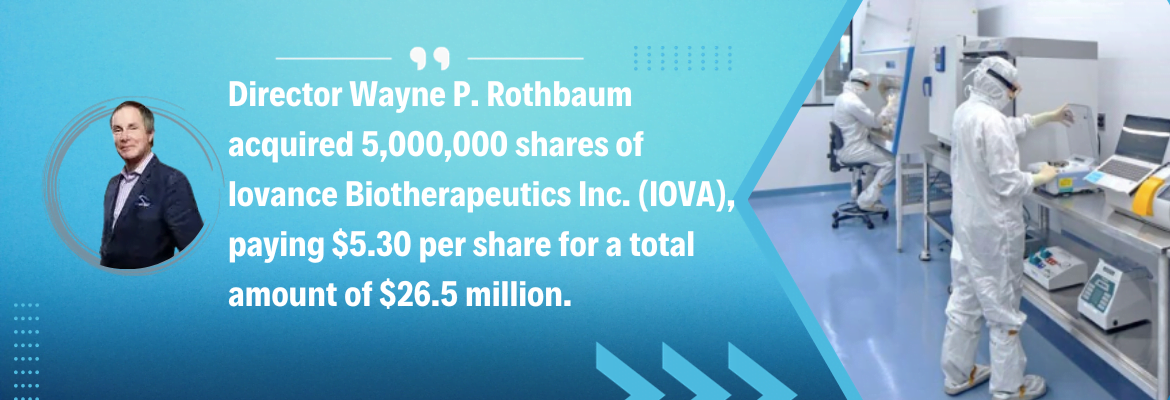

Key Insights Famous biotechnology investor Wayne P. Rothbaum purchased $26.5 million worth of a clinical-stage biotechnology company, Iovance Biotherapeutics Inc. (IOVA). Mr. Rothbaum is well

I was reflecting on the performance of my portfolio during the last several years and realized that beyond opportunistic trades both on the long and

This mid-month update is a couple of days late because I was in Dallas, Texas attending the IDEAS Conference where nearly 60 companies were presenting.

We have created a comprehensive group of tools that allows you to estimate the intrinsic value of investments.